As Congress debates tax rates and potential cuts to entitlements, many Americans face the longer-term reality of a financially uncertain retirement plagued by historically low investment returns, politically-motivated attacks on Social Security and Medicare, and stagnant wages.

Recovery Times To Recoup A Housing Price Loss

Tacoma, Washington (PRWEB) December 13, 2012

As Congress debates tax rates and potential cuts to entitlements, many Americans face the longer-term reality of a financially uncertain retirement plagued by historically low investment returns, politically-motivated attacks on Social Security and Medicare, and stagnant wages.

That’s the prediction from Chuck Epstein, author of the new book, “How 401(k) Fees Destroy Wealth and What Investors Can do To Protect Themselves.” In the book, Epstein writes that a financially secure retirement will elude many Americans since the main wealth-building engines that powered the pre-Baby Boom generations—increases in home equity, portfolio gains, high savings rates, secure pensions and medical entitlement programs–are no longer working for those currently planning to retire.

Here are some specifics, according to Epstein:

Stagnant wages. The decade from 2001 to 2011 saw the smallest wage gains since the Great Depression, according to the U.S. Commerce Department. Worse, the earnings gap between rich and poor Americans was the widest in more than 40 years in 2011, U.S. Census data show. This may help explain why the incomes of the average American family incomes declined last decade for the first time since World War II, according to Bloomberg News.

Low investment returns. This situation is aggravated by the historically low investment returns from U.S Treasuries, the instrument favored by conservative savers. In September, the Federal Reserve announced it would hold interest rates near zero through at least mid-2015. With current Treasury rates less than 0.5%, compared to the historic 3% yield, savers face a difficult time building any significant savings even in a low inflation environment, Epstein said.

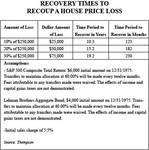

Wealth destruction from losses in home equity. Housing wealth accounts for a majority of total net worth for Baby Boomers, Epstein said. “But the financial losses caused by the housing crisis have vaporized $6 trillion in lost wealth and are expected to destroy an additional $2 trillion. The net impact so far has been the destruction of about $7 trillion m in household net worths. That’s a staggering sue and it could take over a decade to recover from these losses,” Epstein said.

Attacks on pensions and entitlements. What has made the current recession noteworthy is that it has also been accompanied by ideological attacks on pensions, entitlement programs, minimum wage standards and organized labor, Epstein said. “These concerted attacks have added a new degree of financial uncertainty into the retirement planning process that cannot be bridged by traditional calls for personal austerity and strict financial planning,” he said. “Many families already have two wage earners, some working two jobs, yet they are still on shaky financial ground.”

This situation becomes more stressful when employees face threats of layoffs, age discrimination, and a steady stream of new job applicants willing to work for lower wages. This explains why then-Federal Reserve Board Chairman Alan Greenspan said in 1997 that when workers had poor job insecurity, they were more reluctant to ask for raises. This would then eliminate a major cause of inflation, he said.

Threats to privatize Social Security. “This will not only increase financial insecurity among investors, but it will be part of the greatest wealth transfer in the nation’s history,” Epstein said. “Privatizing Social Security will effectively expose millions of ill-equipped investors to the mutual fund industry, which is focused on collecting fees, while evading the fact that the majority of fund managers have very little ability to deliver consistent, above-index market returns that would actually help improve their customers’ lives.”

As an example, he said that in a private Social Security account situation, millions of unsophisticated investors will be paying fees they fail to understand. For example, when investors see that a fund is charging a fee of 1%, they fail to see the fee’s cumulative impact. A General Accounting Office study found that over a 20-year period, each 1% paid in investment fees reduces an investor’s end return by approximately 17%. This draw down is even worse if an investor is also paying their investment adviser an annual management fee of 1% and annual 401(k) fees of 1%. In this situation, an investor’s year-end return is cut by 34%, according to Epstein.

Epstein, who spent over 25 years in the financial services industry, including holding senior marketing positions in the futures industry and at two major mutual fund firms, is the author of “How 401(k) Fees Destroy Wealth and What Investors Can Do To Protect Themselves.”

The book is available on Amazon for $15.95 and Kindle for $9.95. It is 287 pages, with six charts, a glossary and 280 footnotes. ISBN 978-1477657997